WebCab Portfolio for Delphi

- Developer: WebCab Components

- Home page: www.webcabcomponents.com

- License type: Commercial

- Size: 4.39 MB

- Download

Review

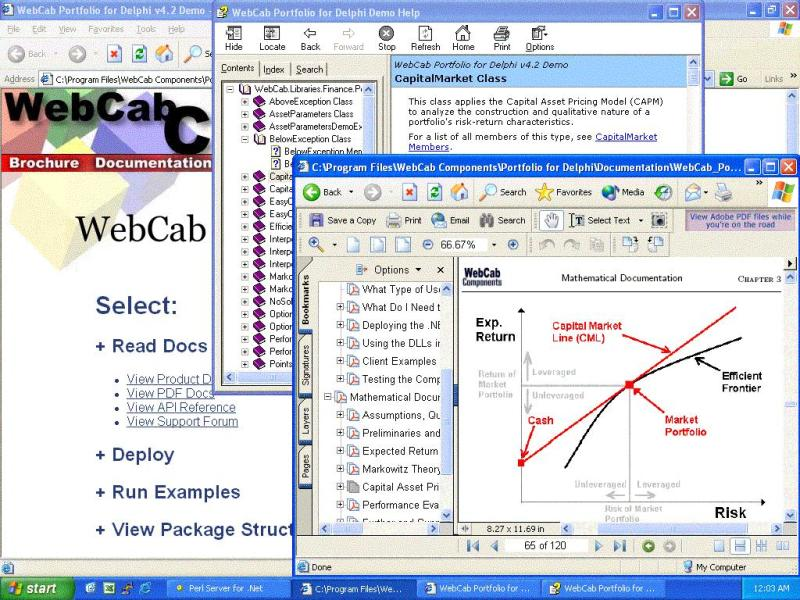

3-in-1: .NET, COM and XML Web service implementation of Markowitz Theory and Capital Asset Pricing Model (CAPM) to analyze and construct the optimal portfolio with/without asset weight constraints with respect to Markowitz Theory by giving the risk, return or investors utility function; or with respect to CAPM by given the risk, return or Market Portfolio weighting. Also includes Performance Evaluation, extensive auxiliary classes/methods including equation solve and interpolation procedures, analysis of Efficient Frontier, Market Portfolio and CML. Utility Functionality included: Interpolation - Cubic spline and general polynomial interpolation procedures to assist in the study of the Efficient Frontier SolveFrontier - Solve the Efficient Frontier with respect to the risk, return, or the investors utility function. MaxRange - Maximum range of the constrained Efficient Frontier AssetParameters - Evaluation of the covariance matrix, expected return, volatility, portfolio risk/variance. Performance Evaluation - Offers a number of procedures for accessing the return and risk adjusted return (Treynors Measure, Sharpes Ratio). This product also has the following technology aspects: 3-in-1: .NET, COM, and XML Web services - Three DLLs, Three API Docs, Three Sets of Client Example all in 1 product. Offering a 1st class .NET, COM, and XML Web service product implementation. Extensive Client Examples - Multiple client examples including .NET (Delphi for .NET, C#, VB.NET), COM and XML Web services (C#, VB.NET) ADO Mediator - The ADO Mediator assists the .NET developer in writing DBMS enabled applications by transparently combining the financial and mathematical functionality of our .NET components with the ADO.NET Database Connectivity model. Compatible Containers (Delphi 3-8, Delphi 2005, C++Builder, C++BuilderX, Office) ASP.NET Web Application Examples ASP.NET Examples with Synthetic ADO.NET