Algo Quant

- Category

- Business

- Misc Financial Tools

- Developer: Numerical Method Inc.

- Home page: numericalmethod.com

- License type: Commercial

- Size: 57.64 MB

- Download

Review

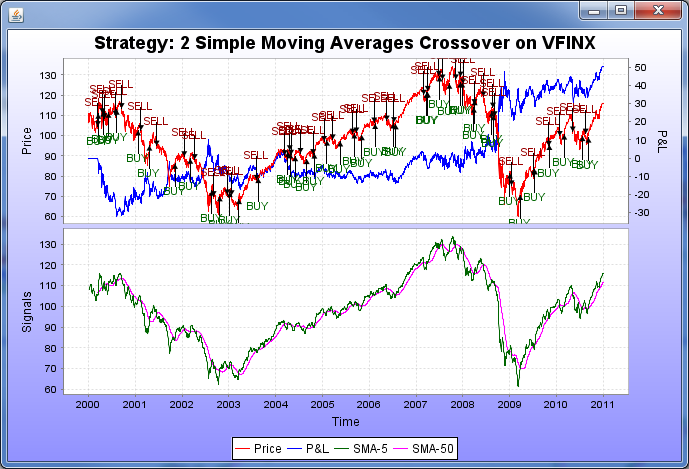

Numerical Method Inc.'s flagship product - Algo Quant - is a library of integrated trading research tools. Algo Quant is a lot more than just an application of backtesting. It is an actively developed and ever more comprehensive library of reusable components that you can use to build your own trading tools from research, backtesting and data analysis to actual automatic order execution. Algo Quant is particularly designed for quantitative and algorithmic trading because it is backed by a very powerful math library (SuanShu), which allows you to very quickly prototype very complicated quantitative strategies. Among other things that Algo Quant does are in-sample calibration and optimization, out-sample backtesting, performance analysis and strategy generation. Algo Quant is written 100% in Java. It runs on all platforms that host a jvm. It is designed from anew using modern software engineering principles. The library contains many reusable components to help you develop trading applications that are solidly object-oriented, unified and testable.